What Credit Score Do You Really Need to Buy in Idaho?

Introduction: Clearing the Confusion Around Credit Scores

If you’re thinking about buying a home in Idaho—whether it’s a new build in Meridian, a resale in Boise, or acreage out in Star or Middleton—you’ve probably heard all kinds of different numbers tossed around about what credit score you “need.” Some say 620. Others insist 700. A few lenders advertise programs that allow you to buy with scores in the 500s. So what’s the real answer?

In this guide, we’ll break down exactly what credit score ranges you need for different loan types in Idaho, how your score affects interest rates and monthly payments, and what you can do if your credit isn’t quite where you want it to be.

Why Your Credit Score Matters When Buying in Idaho

Your credit score is one of the most important factors lenders use to decide whether you qualify for a mortgage and what interest rate you’ll pay. In simple terms:

-

Higher credit score = lower rates and more options.

-

Lower credit score = higher rates and stricter conditions.

That difference can mean hundreds of dollars per month in your mortgage payment—especially in today’s market where Treasure Valley homes average $450,000–$600,000, and new construction communities can push higher.

Minimum Credit Scores by Loan Type

Conventional Loans

-

Minimum Credit Score: 620

-

These are the most common loans in Boise, Meridian, and Eagle, especially for buyers who have solid financial history.

-

Lower down payment options (as little as 3%) are available if you qualify.

FHA Loans

-

Minimum Credit Score: 580 (with 3.5% down)

-

FHA will technically allow scores as low as 500, but then you’ll need 10% down.

-

FHA loans are popular for first-time buyers in Nampa, Kuna, and Caldwell because of their flexibility.

VA Loans (for Veterans)

-

Minimum Credit Score: No set minimum by the VA, but most lenders want 620+.

-

Zero down payment and no mortgage insurance make this one of the best programs out there.

USDA Loans (Rural Areas)

-

Minimum Credit Score: 640 is preferred.

-

Great for buyers in Middleton, Parma, Emmett, or more rural Canyon and Gem County areas.

-

Zero down payment if you qualify.

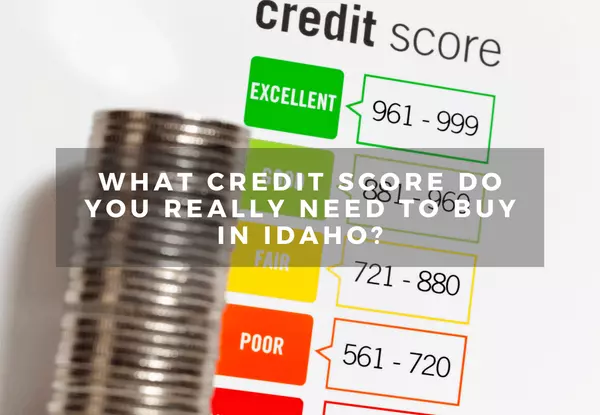

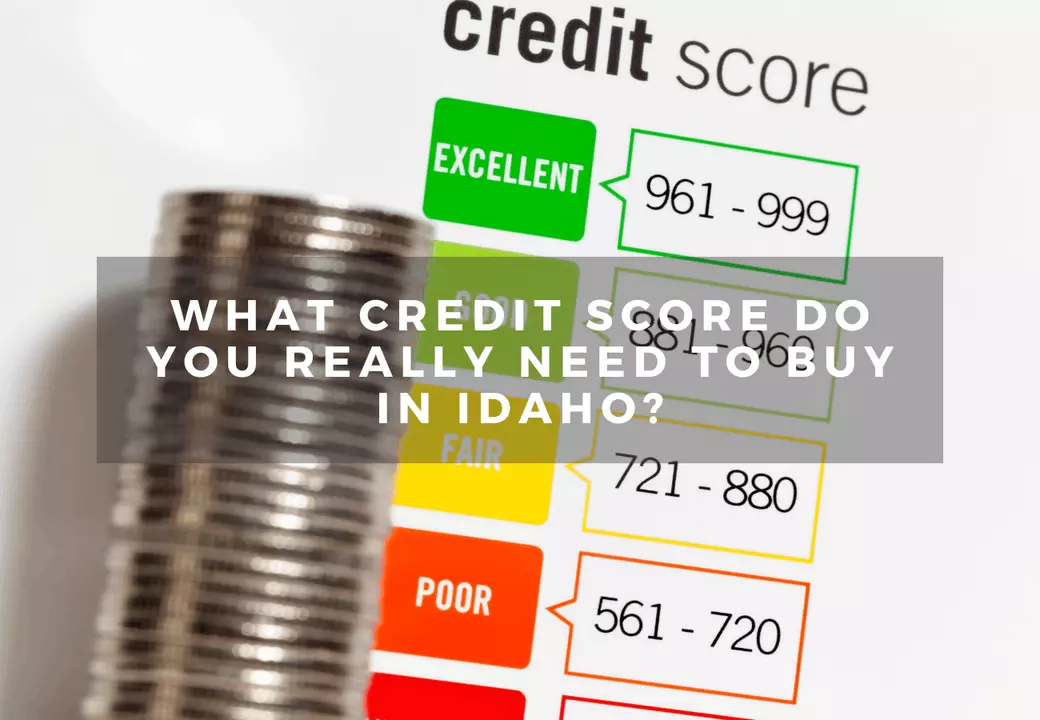

The “Sweet Spot” Credit Score in Idaho

While minimum scores exist, the real question is: what score do you need to get the best deal?

In today’s Idaho market:

-

740+: You’ll usually get the best rates available.

-

700–739: Still very competitive rates.

-

660–699: Doable, but rates will start creeping higher.

-

620–659: You’ll likely qualify, but expect noticeably higher monthly payments.

How Credit Scores Affect Monthly Payments

Let’s say you’re buying a $500,000 home in Meridian. With 5% down:

-

At a 740+ credit score, your rate might be around 6.5%. Monthly payment: ~$3,000 (including taxes/insurance).

-

At a 660 score, your rate could be closer to 7.5%. Monthly payment: ~$3,250.

-

At a 620 score, you might see 8% or higher. Monthly payment: ~$3,500+.

That’s a $500 monthly difference just based on credit score—over $6,000 a year.

Improving Your Credit Before Buying in Idaho

Even a small bump in your credit can save you thousands. Here are steps I’ve seen work well for buyers:

Pay Down Revolving Balances

Keep credit card utilization under 30%—ideally under 10%.

Avoid Opening New Accounts

New accounts can lower your score temporarily due to hard inquiries.

Dispute Errors

Check your credit report for mistakes. Even small errors can drag your score down.

Pay On Time

This is the single biggest factor (35% of your score).

Don’t Let Credit Myths Stop You

I’ve heard from a lot of relocation buyers moving from California, Washington, and Oregon who worry that their credit score isn’t “good enough” for Idaho lenders. Here are some truths:

-

You don’t need an 800 score to buy.

-

Student loans don’t disqualify you. Lenders just factor them into your debt-to-income ratio.

-

Medical debt in collections may not impact your score as heavily as it used to.

Relocation Buyers: How Lenders View Out-of-State Credit

If you’re moving to Idaho, your credit history moves with you. Lenders here don’t treat you differently just because you’re from another state. What matters most is:

-

Your FICO score.

-

Your job history (or transfer letter if you’re relocating).

-

Your debt-to-income ratio.

Local Resources to Help You Boost Credit

If you’re in Treasure Valley and working on your credit, check out:

-

NeighborWorks Boise (neighborworksboise.org) – offers homebuyer education and credit counseling.

-

Idaho Housing and Finance Association (ihfa.org) – down payment assistance and resources.

Activities While House Hunting in Idaho

If you’re flying in to check out homes while working on your credit and loan approval, make it a fun trip too:

-

Boise River Greenbelt (Greenbelt Info) – great for biking and walking.

-

The Village at Meridian (thevillageatmeridian.com) – shopping, dining, movies.

-

Bogus Basin (bogusbasin.org) – skiing in the winter, mountain biking and concerts in the summer.

-

Eagle Saturday Market (eaglemarketplace.org) – local vendors, food, and crafts.

Final Thoughts

Your credit score is important—but it doesn’t have to be perfect to buy in Idaho. Whether you’re relocating for a job, retiring to Eagle, or buying your first home in Nampa, there’s a loan program that fits. The key is knowing where you stand, improving your score where possible, and working with the right lender and Realtor to guide you through the process.

📲 Call or text Curtis Chism at (208) 510-0427

📥 Ready to relocate remotely? Download our Boise Relocation Guide

If you’re thinking about making the move, let’s talk. I’ve helped dozens of families relocate to Boise and the surrounding Treasure Valley, and I’d love to help you too.

Categories

Recent Posts